US Functional Foods Market by Product, Ingredient & Channel 2026–2034

US Functional Foods Market

United States Functional Food Market Size & Forecast (2026–2034)

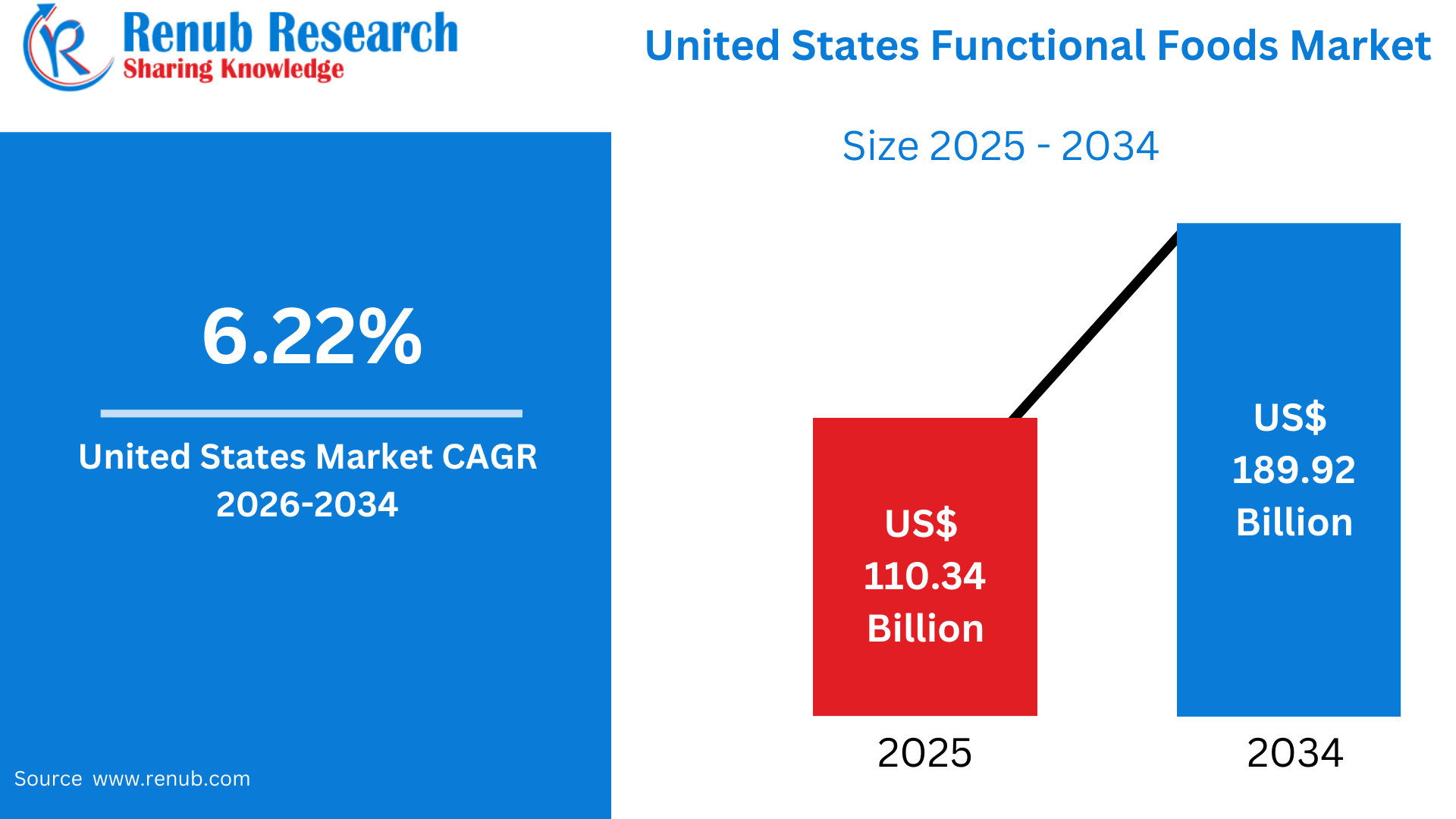

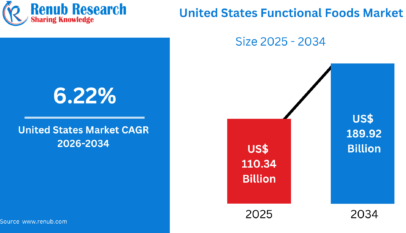

According to Renub Research United States functional food market is poised for strong and sustained growth over the forecast period, driven by rising consumer awareness around nutrition, wellness, and preventive healthcare. The market is projected to expand from US$ 110.34 billion in 2025 to US$ 189.92 billion by 2034, registering a compound annual growth rate (CAGR) of 6.22% from 2026 to 2034. This robust trajectory reflects growing demand for probiotic foods, fortified beverages, protein-rich snacks, and natural health-enhancing ingredients that align with evolving consumer lifestyles and health priorities.

Functional foods have moved well beyond niche health segments to become a mainstream component of American diets. Consumers increasingly perceive food not only as nourishment but also as a proactive tool to support immunity, digestion, heart health, cognitive performance, and overall well-being. This structural shift in food consumption behavior underpins the long-term expansion of the U.S. functional food market.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=united-states-functional-foods-market-p.php

United States Functional Food Market Outlook

Functional foods are defined as food products that deliver health benefits beyond basic nutrition. These benefits are typically derived from bioactive compounds such as probiotics, prebiotics, vitamins, minerals, antioxidants, omega-3 fatty acids, plant extracts, and specialty proteins. Common examples include fortified breakfast cereals, probiotic yogurts, omega-3–enriched eggs, protein bars, kombucha, plant-based functional beverages, and fiber-enriched foods.

In the United States, functional foods have gained immense popularity due to heightened health awareness and a strong cultural shift toward preventive wellness. Consumers are increasingly focused on managing stress, improving gut health, enhancing immunity, and maintaining consistent energy levels through everyday dietary choices. Rather than relying solely on supplements or medications, many Americans prefer food-based solutions that integrate seamlessly into daily routines.

Convenience remains a critical factor in adoption. Ready-to-eat and ready-to-drink functional foods appeal strongly to busy professionals, students, parents, and fitness-conscious individuals. Additionally, the growing popularity of plant-based diets, clean-label products, and natural ingredients has accelerated acceptance of functional foods across demographics. With supermarkets, online retailers, and foodservice operators rapidly expanding their functional food portfolios, these products are now firmly embedded in mainstream U.S. consumption patterns.

Growth Drivers in the United States Functional Food Market

Increasing Health Awareness and Preventive Wellness

One of the most influential drivers of the U.S. functional food market is the growing emphasis on preventive health, longevity, and holistic wellness. Aging demographics, rising prevalence of chronic lifestyle-related conditions, and escalating healthcare costs have collectively encouraged consumers to adopt proactive health management strategies.

Functional foods offer a low-friction solution by enabling consumers to address specific health needs through regular meals and snacks. Products such as fortified cereals for micronutrient intake, probiotic yogurts for digestive health, omega-3–enriched foods for cardiovascular support, and botanically enhanced beverages for stress management have gained widespread acceptance. This shift from reactive treatment to daily prevention continues to expand the consumer base for functional foods.

Innovation in Formulation and Sensory Experience

Product innovation is a key factor driving repeat purchases and category expansion. Early functional foods often faced adoption barriers due to compromises in taste, texture, or mouthfeel. Today, advancements in food science allow manufacturers to combine functional efficacy with enjoyable sensory experiences.

Modern research and development focuses on blending probiotics, adaptogens, dietary fiber, peptides, and plant-based proteins with advanced delivery systems that maintain ingredient stability and bioavailability. Techniques such as microencapsulation, natural flavor systems, and plant-based carriers enable the creation of indulgent formats including smoothies, snack bars, crisps, and ready-to-drink beverages. Multi-benefit formulations—such as protein combined with probiotics and vitamin D—further enhance product appeal by addressing multiple wellness goals in a single offering.

Channel Expansion and Personalized Digital Commerce

The expansion of distribution channels has significantly improved consumer access to functional foods. In addition to traditional supermarkets and pharmacies, functional products are increasingly available through specialist wellness retailers, fitness centers, subscription services, and e-commerce platforms.

Digital commerce has emerged as a particularly powerful growth engine. Online channels allow brands to collect first-party consumer data, offer personalized recommendations, and deploy subscription models that improve retention. Integration with mobile applications and digital nutrition platforms enables customized product bundles based on dietary preferences, health goals, and lifestyle data. Strategic retail partnerships, sampling initiatives, and targeted digital advertising further accelerate product discovery and adoption.

Challenges in the United States Functional Food Market

Regulatory Ambiguity and Evidence Expectations

Regulatory complexity remains a major challenge for the functional food industry. Functional foods sit between conventional foods and dietary supplements, creating ambiguity around permissible health claims, ingredient approvals, and labeling requirements at both federal and state levels.

Consumers increasingly demand clinically supported and transparent health claims, but generating robust human clinical evidence is costly and time-consuming. Marketing communications must be carefully structured to avoid implied disease treatment claims that could trigger regulatory action. Smaller brands often struggle with the financial and technical resources required to meet evolving evidence expectations, while larger companies face reputational risks if products fail to meet consumer expectations.

Ingredient Sourcing, Cost Pressures, and Supply Chain Risk

Securing consistent, high-quality functional ingredients is another key challenge. Inputs such as probiotics, botanical extracts, specialty proteins, and omega-3 concentrates are subject to agricultural variability, geopolitical factors, and concentrated supplier bases. These factors contribute to raw material price volatility and margin pressure.

Supply chain disruptions—caused by climate events, transportation delays, or capacity constraints—can interrupt product availability and erode brand trust. Additionally, increasing expectations around traceability, sustainability, and ethical sourcing require ongoing investment in supplier audits, certifications, and diversified sourcing strategies. Smaller manufacturers are particularly vulnerable due to limited negotiating power and reliance on single-source suppliers.

United States Breakfast Cereals Functional Food Market

Functional breakfast cereals have evolved from basic vitamin fortification to targeted nutrition platforms. Modern formulations include probiotics, prebiotic fiber, plant-based proteins, omega-3 fatty acids, and botanicals designed to support immunity, gut health, sustained energy, and cognitive focus.

Manufacturers are repositioning breakfast as a therapeutic nutrition occasion, offering blends that stabilize blood sugar, provide slow-release energy, and address age-specific nutritional needs. Product innovation emphasizes whole grains, reduced added sugar, and clean-label ingredients. Convenient single-serve and on-the-go formats cater to busy households, while retailer shelf segmentation and influencer partnerships drive consumer trial.

United States Baby Functional Food Market

The baby functional food segment targets parents seeking enhanced nutrition for infants and toddlers beyond basic feeding requirements. Products include fortified baby cereals, DHA-enriched purees, probiotic toddler snacks, and prebiotic-enhanced formulas that support digestive and immune development.

Trust is paramount in this category. Parents prioritize transparent ingredient sourcing, strict safety standards, allergen control, and age-appropriate dosing. Brands often highlight pediatric endorsements, clinical research, and rigorous manufacturing controls to build credibility. Packaging innovations such as resealable pouches and portion-controlled servings add convenience, while marketing focuses on developmental milestones such as brain development, immunity, and digestive comfort.

United States Probiotics Functional Food Market

Probiotic functional foods have transitioned from niche offerings to mainstream staples in the U.S. market. Beyond yogurt, probiotics are now widely incorporated into beverages, snack bars, cereals, and shelf-stable shots.

Consumer interest is driven by growing awareness of the gut–immune and gut–brain connections. Differentiation among brands is based on strain specificity, colony-forming unit (CFU) counts, survivability through shelf life and digestion, and delivery technology. Products that communicate strain-level evidence and consumer-relevant outcomes—such as improved bowel regularity or immune resilience—tend to command higher trust and premium positioning.

United States Vitamins Functional Food Market

Vitamin-enriched functional foods have shifted from generic fortification to targeted, occasion-based nutrition. Products address specific needs such as energy support, immune defense, mood balance, and bone health through cereals, beverages, snack bars, gummies, and powdered mixes.

Consumers increasingly prefer naturally derived vitamins, enhanced bioavailability, and transparent labeling. Manufacturers are responding with chelated minerals, liposomal delivery systems, and combination formulations designed to improve absorption. Vitamin functional foods are often merchandised alongside supplements, while digital channels enable convenient subscription-based purchasing.

United States Functional Food Specialist Retailers Market

Specialist retailers—including natural food stores, health grocers, and wellness boutiques—play a vital role in the functional food ecosystem. These outlets curate high-quality and niche brands, emphasize third-party certifications, and provide consumer education through knowledgeable staff and in-store demonstrations.

Specialist retailers often act as trend accelerators, introducing emerging concepts such as plant-based proteins, adaptogens, and clean-label superfoods before they reach mass-market adoption. They also serve as incubation platforms for smaller brands seeking regional or national exposure.

United States Functional Food Online Market

E-commerce has transformed functional food distribution by enabling direct consumer engagement and personalized shopping experiences. Online platforms allow brands to communicate detailed ingredient stories, usage guidance, and scientific references—critical elements for building trust in functional categories.

Advanced algorithms support personalized product recommendations based on consumer behavior and health goals, while social commerce amplifies influencer-driven launches. Improvements in cold-chain logistics have expanded online availability of fresh functional products such as probiotic beverages and wellness shots, enabling national reach without extensive brick-and-mortar investment.

United States Sports Nutrition Market

The sports nutrition segment is one of the most dynamic areas within the functional food market. Growth is driven by rising gym participation, endurance sports, home fitness adoption, and a broader cultural emphasis on active lifestyles.

Products focus on muscle recovery, performance enhancement, hydration, and joint health, with innovation centered on high-quality proteins, BCAAs, collagen blends, electrolytes, and low-sugar formulations. Plant-based sports nutrition options have broadened appeal beyond traditional athletes to mainstream consumers. Ingredient transparency, third-party testing, and clear labeling are particularly important for this segment.

State-Level Market Insights

California Functional Food Market

California leads functional food innovation and adoption due to its strong wellness culture, robust startup ecosystem, and large base of health-conscious consumers. Demand is high for plant-based, clean-label, and sustainably sourced functional foods. The state’s ecosystem of ingredient suppliers, research institutions, and venture capital accelerates product development and market entry.

New York Functional Food Market

New York’s functional food market benefits from a diverse consumer base, rapid uptake of new concepts, and a dense retail and foodservice network. Busy urban lifestyles support demand for grab-and-go functional meals, probiotic beverages, and fortified bakery items. Media exposure, influencer culture, and corporate wellness programs further amplify product visibility and adoption.

Market Segmentation

By Product Type:

Bakery Products, Breakfast Cereals, Snacks and Functional Bars, Dairy Products, Baby Food, Others

By Ingredient:

Probiotics, Minerals, Proteins and Amino Acids, Prebiotics and Dietary Fiber, Vitamins, Others

By Distribution Channel:

Supermarkets and Hypermarkets, Specialist Retailers, Convenience Stores, Online Stores, Others

By Application:

Sports Nutrition, Weight Management, Clinical Nutrition, Cardio Health, Others

By Top States:

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, and others

Competitive Landscape and Company Analysis

The U.S. functional food market is highly competitive and innovation-driven. Key players include Abbott Laboratories, Amway, BASF SE, Cargill Incorporated, Clif Bar & Company, Danone S.A., General Mills Inc., Kellogg Company, Kerry Group Plc., and Nestlé S.A..

Each company is analyzed across overview, key leadership, recent developments, SWOT analysis, and revenue performance, highlighting strategies focused on innovation, clean-label positioning, and omnichannel expansion.

Conclusion

The United States functional food market is set for strong, long-term growth through 2034 as consumers increasingly integrate nutrition, wellness, and preventive health into everyday eating habits. While regulatory complexity and supply chain challenges persist, continuous innovation, digital commerce expansion, and rising health awareness ensure a positive outlook. Functional foods are no longer a niche category but a foundational element of the modern American food landscape, offering significant opportunities for both established players and emerging brands.

Easy tips and tricks to clean your sofa at home

The sofa is the center of your living space. Your sofa is a place where … …

Fun Online Entertainment Experience

KP88 – A Comprehensive Look at a Popular Online Gaming Platform Introduction to KP88 …

{kind=link}